Variable interest rate on a home equity line of credit

Home equity credit can be used to borrow against your equity and is useful for large-scale projects. It can also be risky, especially if interest rates fluctuate. It is essential to be able to tell the difference between fixed-rate HELOCs and variable-rate HELOCs. A fixed rate HELOC is only available for a limited time. A variable-rate HELOC offers unlimited borrowing options.

There are many factors that affect how much you can borrow on a line of credit for home equity. Quick calculations can give you an idea of how much you can borrow.

Fixed-rate loan secured with your home

Fixed-rate loans that are secured by your home can be made if there is equity in your house. This loan is ideal for those who need a large lump sum of money but know exactly how much. They can use the money for almost anything, including home improvements. You can also deduct the interest from your income taxes.

Fixed-rate home equity loans are secured by your home's equity. The interest rate is linked to an independent benchmark such as the U.S. prime rate, currently at 3.5 percent. While most lenders require a minimum credit score requirement of 620, some lenders have higher requirements. A higher credit score will allow you to get a lower rate of interest.

Maximum amount that you can borrow

A home equity loan allows you to borrow up 80 percent of your home's equity. This amount is also known by the maximum amount you may borrow with a credit card (HELOC) for home equity. This loan is available to you for home improvements that will increase your home's value. However, there are a few factors to consider before borrowing against your home.

First, your credit score and income will impact how much you can borrow. You may not be eligible for a home equity loan if you have a low income. High upfront fees may also apply to home equity loans. These fees could reduce the amount you can borrow.

There are some downsides to a loan for home equity

A home equity loan is a great option if you are interested in borrowing money against your home's value. The best thing about home equity loans is that they don't put your home at danger. It is essential that you are able to repay any money you borrow. Keep a track of your incomes and expenses to help you prepare. You will be able to determine if you can afford your new payment. The process of applying to a home equity mortgage is easy, but it's not guaranteed that you will be approved.

The interest rate on home equity loans is also lower than other financial products. Although the interest rate depends on your creditworthiness and other factors, it is generally lower that a credit card or an unsecure personal loan. The tax deduction for home equity loans is another advantage. Depending on your credit score, a home equity loan can help you lower your tax bill. And unlike a credit card or unsecured personal loan, interest on a home equity loan can be reinvested into your home.

FAQ

What should I do if I want to use a mortgage broker

A mortgage broker is a good choice if you're looking for a low rate. Brokers work with multiple lenders and negotiate deals on your behalf. Brokers may receive commissions from lenders. Before you sign up, be sure to review all fees associated.

Is it better buy or rent?

Renting is usually cheaper than buying a house. It is important to realize that renting is generally cheaper than buying a home. You will still need to pay utilities, repairs, and maintenance. Buying a home has its advantages too. You will be able to have greater control over your life.

How do I calculate my interest rate?

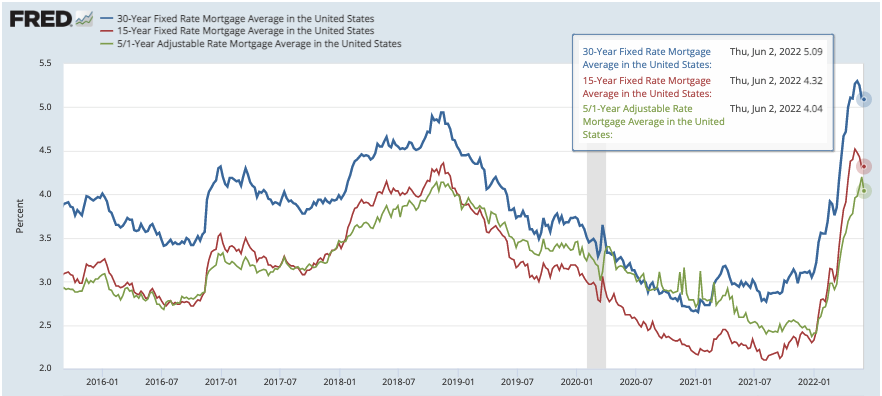

Market conditions affect the rate of interest. The average interest rates for the last week were 4.39%. The interest rate is calculated by multiplying the amount of time you are financing with the interest rate. For example, if $200,000 is borrowed over 20 years at 5%/year, the interest rate will be 0.05x20 1%. That's ten basis points.

What is a reverse loan?

A reverse mortgage allows you to borrow money from your house without having to sell any of the equity. It allows you to borrow money from your home while still living in it. There are two types to choose from: government-insured or conventional. You must repay the amount borrowed and pay an origination fee for a conventional reverse loan. FHA insurance covers your repayments.

What should I look for in a mortgage broker?

People who aren't eligible for traditional mortgages can be helped by a mortgage broker. They shop around for the best deal and compare rates from various lenders. Some brokers charge a fee for this service. Others offer free services.

How can I determine if my home is worth it?

It could be that your home has been priced incorrectly if you ask for a low asking price. You may not get enough interest in the home if your asking price is lower than the market value. For more information on current market conditions, download our Home Value Report.

Do I need flood insurance?

Flood Insurance covers flooding-related damages. Flood insurance helps protect your belongings and your mortgage payments. Learn more about flood coverage here.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How to Find Real Estate Agents

Real estate agents play a vital role in the real estate market. They can sell properties and homes as well as provide property management and legal advice. You will find the best real estate agents with experience, knowledge and communication skills. Online reviews are a great way to find qualified professionals. You can also ask family and friends for recommendations. Consider hiring a local agent who is experienced in your area.

Realtors work with residential property sellers and buyers. It is the job of a realtor to help clients sell or buy their home. As well as helping clients find the perfect home, realtors can also negotiate contracts, manage inspections and coordinate closing costs. A majority of realtors charge a commission fee depending on the property's sale price. Some realtors do not charge fees if the transaction is closed.

The National Association of Realtors(r), (NAR), has several types of licensed realtors. NAR members must pass a licensing exam and pay fees. Certification is a requirement for all realtors. They must take a course, pass an exam and complete the required paperwork. NAR designates accredited realtors as professionals who meet specific standards.