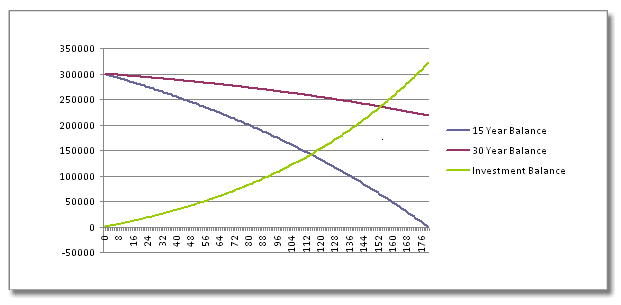

When deciding between a personal loan and a home equity loan, it is important to understand the pros and cons of both types. A personal loan usually has higher interest rates, higher monthly payments, and a home loan has a lower interest-rate and monthly payment. A home equity loans can be an excellent option to help you make improvements in your home and get rid of credit card debt.

Low monthly payments on home equity loans

Home equity loans tend to have lower monthly payments that personal loans. To take advantage of this advantage you will need to meet several requirements. First, you need to have at least 15% equity in your home. You must also have sufficient income. The second is to have a low level of debt-to income (DTI). Borrowers with a DTI less than 43% are preferred by lenders. Good credit scores are also important. Higher credit scores will result in higher interest rates.

A home equity mortgage can allow you to borrow as much as 80% of your home's equity. Home equity loans are available to those with good credit ratings and minimal debt. You could get as much as $100,000. This loan cannot be repaid in full. Also, the process is longer. Home equity loans, unlike personal loans, will take longer to receive funds.

Personal loans have higher interest rate

There are many things that differ between a loan for personal use and a loan for home equity. Personal loans are secured. This means that the lender cannot seize your property if it defaults on the loan. To qualify for a home equity loan, however, you will need to have enough equity in your house. People with bad credit or insufficient equity may not be eligible for a home equity loan. Personal loans may be an option in this situation.

Personal loans usually carry higher interest rates than home equity loans. This is because they are riskier for lenders. Borrowers with a minimum credit score of 780 are eligible for an 8.83% personal loan. Also, personal loan interest rates include origination fees, which can be anywhere from 1% to 8% of the loan amount.

Home equity loans offer a great choice for home improvements

A home equity mortgage is a great way of funding your home improvement projects. This loan will help you make improvements to your home and increase it's value. The loan will allow you to reap the benefits as long you pay the monthly payments.

Although home equity loans can be a good option for home improvement, you should consider the pros and cons of them before applying. First of all, remember that defaulting in repayment on your loan can result in losing your home. Your credit score is key to avoiding foreclosure. This can be done by paying your bills on time, paying down all debt, and disputing any negative marks on your credit. You can make your house more valuable and sell it faster by renovating.

Home equity loans offer a great way to get rid of credit card debt

Home equity loans offer a great option to reduce credit card debt because they are lower in interest than many credit cards. You can use them to consolidate multiple credit cards balances and make it easier to track your payments. However, home equity loans are not without their downsides.

Good credit is required to get home equity loans. You will be required to pay a higher rate of interest if your credit is not good. You can deduct the interest from a home equity mortgage if you make home improvements. To determine if a loan for home equity is right for your situation, consult a tax professional.

FAQ

Can I get another mortgage?

Yes, but it's advisable to consult a professional when deciding whether or not to obtain one. A second mortgage can be used to consolidate debts or for home improvements.

How many times can my mortgage be refinanced?

This will depend on whether you are refinancing through another lender or a mortgage broker. You can typically refinance once every five year in either case.

Is it possible to sell a house fast?

It might be possible to sell your house quickly, if your goal is to move out within the next few month. Before you sell your house, however, there are a few things that you should remember. You must first find a buyer to negotiate a contract. Second, prepare the house for sale. Third, your property must be advertised. Finally, you need to accept offers made to you.

Can I purchase a house with no down payment?

Yes! Yes. There are programs that will allow those with small cash reserves to purchase a home. These programs include FHA loans, VA loans. USDA loans and conventional mortgages. More information is available on our website.

Is it better to buy or rent?

Renting is often cheaper than buying property. However, you should understand that rent is more affordable than buying a house. A home purchase has many advantages. You'll have greater control over your living environment.

What is a "reverse mortgage"?

Reverse mortgages are a way to borrow funds from your home, without having any equity. It works by allowing you to draw down funds from your home equity while still living there. There are two types of reverse mortgages: the government-insured FHA and the conventional. If you take out a conventional reverse mortgage, the principal amount borrowed must be repaid along with an origination cost. FHA insurance covers your repayments.

Statistics

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

External Links

How To

How to Find Houses To Rent

Renting houses is one of the most popular tasks for anyone who wants to move. Finding the perfect house can take time. Many factors affect your decision-making process when choosing a home. These factors include size, amenities, price range, location and many others.

You should start looking at properties early to make sure that you get the best price. Ask your family and friends for recommendations. This will ensure that you have many options.