Use a home affordability calculator to see if you are able afford a property purchase. This calculator allows you to input many factors such as down payment, interest rates, and property taxes. The results will be calculated based upon your credit score and other factors. The results can vary depending on the market, lender guidelines and mortgage selection. Remember that these results can be rounded up or decreased and may not reflect the actual result.

Down payment

The affordable loan calculator allows you to calculate the down payment that you can afford. The calculator calculates the price of a house based on your gross monthly earnings, down payment, debt, and other factors. The down payment amount is one of the most important factors that determine affordability.

The down payment calculator can be especially useful if your budget is not clear and you don't know how much money you have available. You can enter the price of the home that you are interested in buying and the calculator will automatically calculate how much your down payment. You can also adjust the homeowners insurance rate or amount that will be added to your mortgage payment.

Your credit score plays an important role in your financial situation and can affect your mortgage rate. A credit score of 740 and higher will help you secure the best interest rate and lowest monthly payment on your home loan. A low credit score could result in $300 less monthly mortgage payments. You can check your credit score at one of three agencies.

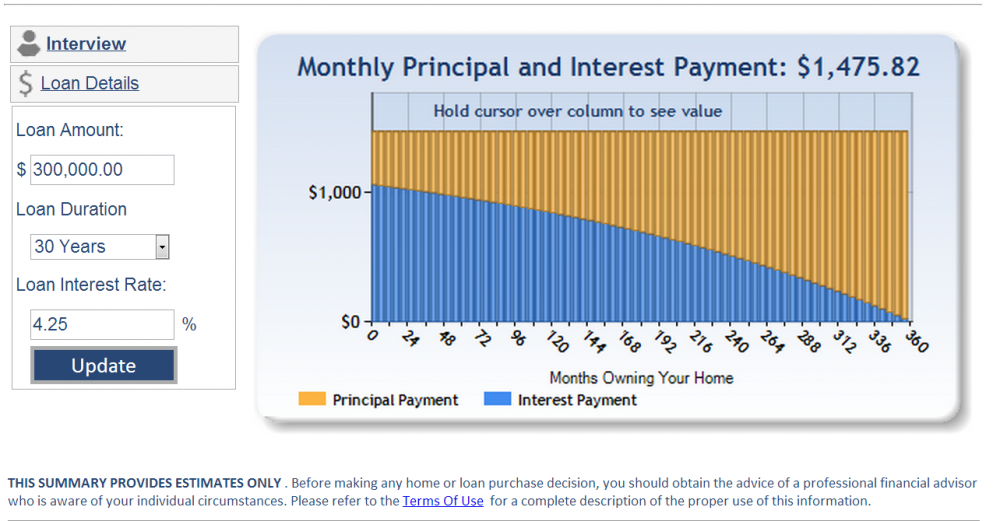

Rate of interest

It is important to take into account the interest rate when you choose a home loan. The interest rates represent a percentage the total loan balance. The affordability calculator will use an average national mortgage rate to calculate the rate you will pay. However your exact rate will differ depending on factors like your down payment.

The next step after you have determined the interest rate is to calculate your monthly payment. The affordability calculator will take into account the total payment, which includes the interest rate, property taxes, and homeowner's insurance. This information can be used to calculate the range of home prices that you are able to afford once you have determined your budget.

Property taxes

You will need to determine how much property taxes are going to cost if you buy a house. It will vary depending on the location and value of your house. To find out how much you will need to pay, do your research online. Or ask a realty agent. Most homeowners pay their taxes using an escrow account attached to their mortgage payments. In property taxes, a $100,000 home would be worth $1,000 per annum.

A property tax calculator can give you the average annual tax rate in your region. These rates can vary significantly between counties and between states. For example, property taxes can increase the cost of a New Jersey house by more than one per cent, while Wyoming homes will have a lower cost.

FAQ

What are the advantages of a fixed rate mortgage?

Fixed-rate mortgages allow you to lock in the interest rate throughout the loan's term. This means that you won't have to worry about rising rates. Fixed-rate loans come with lower payments as they are locked in for a specified term.

What should I look out for in a mortgage broker

People who aren't eligible for traditional mortgages can be helped by a mortgage broker. They search through lenders to find the right deal for their clients. This service is offered by some brokers at a charge. Others provide free services.

What can I do to fix my roof?

Roofs may leak from improper maintenance, age, and weather. Roofing contractors can help with minor repairs and replacements. Contact us for further information.

How can you tell if your house is worth selling?

It could be that your home has been priced incorrectly if you ask for a low asking price. You may not get enough interest in the home if your asking price is lower than the market value. Our free Home Value Report will provide you with information about current market conditions.

Statistics

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to become real estate broker

An introductory course is the first step towards becoming a professional real estate agent. This will teach you everything you need to know about the industry.

The next step is to pass a qualifying examination that tests your knowledge. This involves studying for at least 2 hours per day over a period of 3 months.

This is the last step before you can take your final exam. To be a licensed real estate agent, you must achieve a minimum score of 80%.

If you pass all these exams, then you are now qualified to start working as a real estate agent!