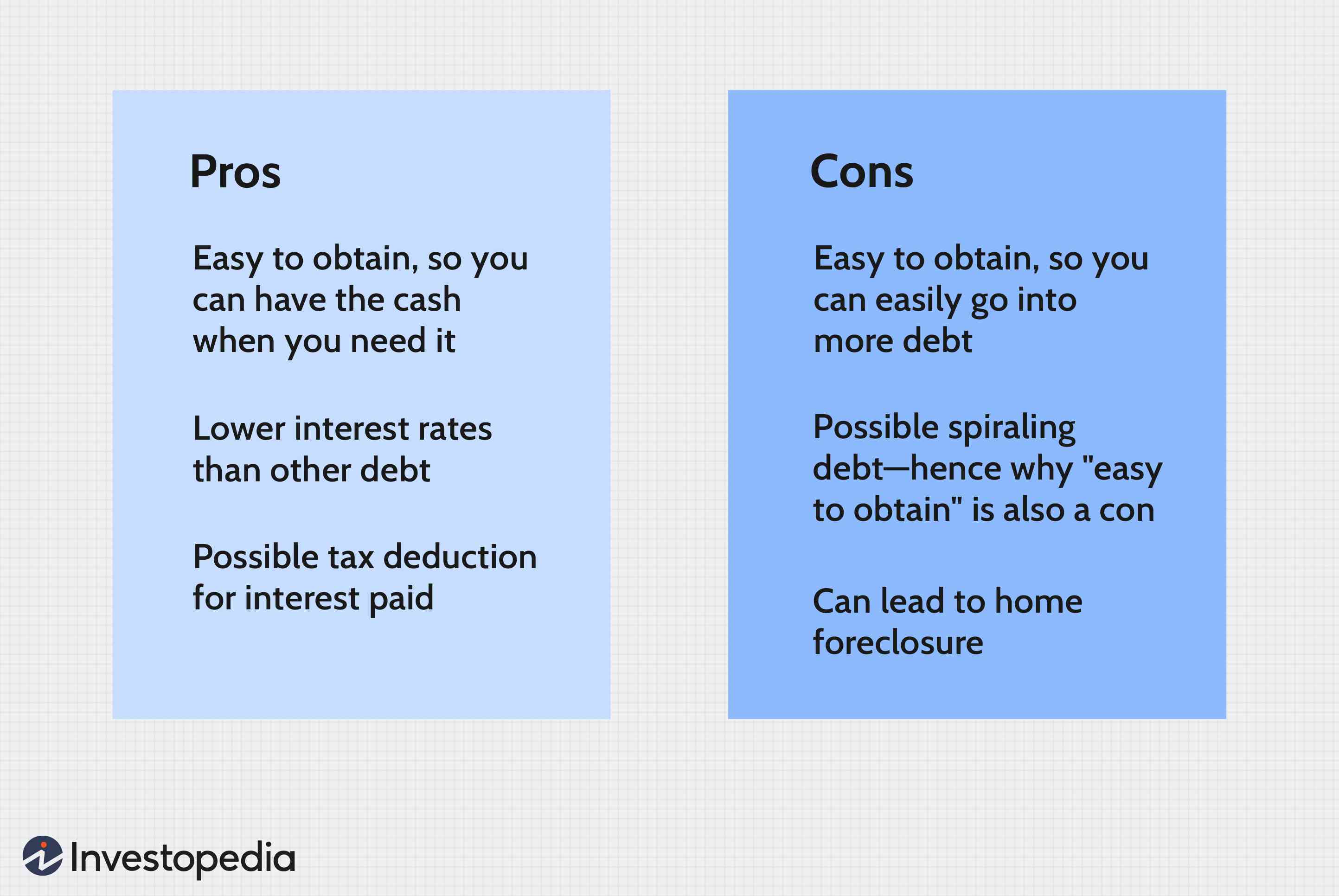

The IRS has always denied PMI tax deductions. However, new legislation has reinstated the deductions. The Further Consolidated Appropriations Act of 2020 permits people to make PMI taxes deductions retroactively for 2018 and 2019, respectively. People who did not claim PMI deductions in 2018 may still be eligible for them in 2019. They must file an amended form and wait three years to claim the deductions. The deduction was extended to the end of 2021. However, Congress could extend it in the future.

Lender-paid PMI

Lender-paidPMI (LPMI), also known as mortgage insurance, is rolled into your mortgage rates and tax deductible. You may be able, if you itemize income taxes to the extent that you can deduct the cost LPMI. The deduction is eliminated if your household's income is less than $100,000. Borrower-paid PMI may be more advantageous for you.

PMI typically costs between $30 and $70 per $100,000 borrowed money. Your homeowner's insurance and mortgage will also be covered. You'll need to pay between $996-$2316 per annum. Good news: The federal tax deduction for this expense has been reinstated in late 2019. It will be extended through 2021.

There are many reasons why LPMI is cheaper for borrowers. However, the most popular reason is that it lowers monthly payments and makes it easier for borrowers to qualify for a mortgage. You're also more likely to sell your house if you are a first-time home buyer.

Standard deduction

You may wonder if it is possible to deduct private mortgage insurance payments. Your annual income is one factor that will determine your eligibility. PMI is not available to those who earn less than $54,500. If you make more than that, you will only be able to take the standard deduction.

This deduction will remain in effect through the year 2022. You may also be able to deduct mortgage insurance from previous years if you meet certain conditions. Paying down your mortgage is the best way to make sure you are able to continue to take a PMI deduction. At least 20% equity should be in your home.

Only homeowners who itemize their deductions are eligible for the PMI deduction. It is possible that you will not be eligible. First, homeowners with $100,000 mortgages are not eligible for the deduction. To get the full amount, you will have to pay $50 per $100,000. The actual amount depends on the type of loan and down payment that you made.

Income phaseouts

You may be eligible to receive a tax deduction if you are paying PMI on your house. However, your deduction is limited and will begin to phase out once your adjusted gross income (AGI) exceeds a certain threshold. If you earn $100,000, but file separately, your PMI premiums can be deducted only $54,500. If you make less that $109,000, however, you can deduct 100%. This applies to both home purchases as well as refinancing transactions.

The deduction for PMI, which was originally suspended in 2017, was reinstated in the latter part of 2019. This was retroactively applied for the 2018 tax year, and extended into the 2021 tax season. PMI should not be deducted if you don't have the funds to pay the monthly premiums.

FAQ

What are the advantages of a fixed rate mortgage?

Fixed-rate mortgages allow you to lock in the interest rate throughout the loan's term. This will ensure that there are no rising interest rates. Fixed-rate loans offer lower payments due to the fact that they're locked for a fixed term.

What should I do before I purchase a house in my area?

It depends on the length of your stay. Save now if the goal is to stay for at most five years. But if you are planning to move after just two years, then you don't have to worry too much about it.

Can I get another mortgage?

However, it is advisable to seek professional advice before deciding whether to get one. A second mortgage can be used to consolidate debts or for home improvements.

How much will my home cost?

It depends on many factors such as the condition of the home and how long it has been on the marketplace. Zillow.com shows that the average home sells for $203,000 in the US. This

Do I need flood insurance

Flood Insurance protects from flood-related damage. Flood insurance helps protect your belongings, and your mortgage payments. Find out more information on flood insurance.

Statistics

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

External Links

How To

How to Buy a Mobile Home

Mobile homes can be described as houses on wheels that are towed behind one or several vehicles. They were first used by soldiers after they lost their homes during World War II. People who want to live outside of the city are now using mobile homes. There are many options for these houses. Some houses are small while others can hold multiple families. There are some even made just for pets.

There are two types of mobile homes. The first is built in factories by workers who assemble them piece-by-piece. This takes place before the customer is delivered. You can also build your mobile home by yourself. You'll need to decide what size you want and whether it should include electricity, plumbing, or a kitchen stove. Next, make sure you have all the necessary materials to build your home. To build your new home, you will need permits.

These are the three main things you need to consider when buying a mobile-home. First, you may want to choose a model that has a higher floor space because you won't always have access to a garage. Second, if you're planning to move into your house immediately, you might want to consider a model with a larger living area. You should also inspect the trailer. You could have problems down the road if you damage any parts of the frame.

Before buying a mobile home, you should know how much you can spend. It is important to compare the prices of different models and manufacturers. Also, take a look at the condition and age of the trailers. Many dealers offer financing options. However, interest rates vary greatly depending upon the lender.

An alternative to buying a mobile residence is renting one. Renting allows for you to test drive the model without having to commit. Renting is expensive. Renters usually pay about $300 per month.