You should do your research thoroughly before buying a pre-foreclosure home. There are several ways to do this. The first step is to find out why the property was pre-foreclosed. The second step involves a physical inspection of the property. The third stage involves thorough review of all legal documents and the down payment. If you don't have enough money for the down payment, there are hard-money loan lenders that can help you. You should also know the total amount of expenses that you have incurred over the past year.

Options to stop a pre-foreclosure

Although the foreclosure process can be difficult, there are ways to stop it. Negotiate with the lender for loan modification. This will allow your payments to be reduced over a longer term. Once you have reached an agreement on a loan modification, it is possible to stop the foreclosure process and not have to sell your home. If you don't agree to a loan modification, your lender can pursue a foreclosure auction to collect the remainder of your loan.

Filing for bankruptcy is another option to stop pre-foreclosures. Most of the time, bankruptcy will make you insolvent. This will also stop the foreclosure process. But, if you do not have this option, your lender could offer other options like loan modifications.

Steps to take during this process

It is important to be informed about your options if you are currently in the preforeclosure process. Pre-foreclosure is avoidable if you pay your debts early. You will most likely be able buy pre-foreclosure property for a fraction of the amount you owe to your lender. You should do your homework before you make any offers. Due diligence includes all aspects of purchasing a preforeclosed property, including the legal, financial and physical. Financial due diligence includes looking at the down payment and mortgage payments you have made on your home. Also, you should have your income and expenses from the last year verified.

Selling your pre-foreclosure property is another option. This option saves the bank money and time by avoiding the foreclosure process entirely. However, it's still risky since it could fall through before the pre-foreclosure sale is completed. In the event that the sale does not go through, your deposit could be forfeited. Also, the seller may have the right to refuse your offer or cancel the transaction.

Common lenders involved

There are two main types of lenders involved in pre foreclosure. First, conventional lenders and hard-money lenders. Hard money lenders will help you buy a property if it is in default. They don't care as much about a borrower’s credit score, but are more concerned about a property's potential profitability. Rentability is determined by the property's value after repair.

These investors can purchase properties that are in foreclosure for less money than their lender owes. They should also be aware that traditional lenders will not approve these loans. Instead, they should apply for a hard cash loan. If that fails, they can try to get a loan from a different hard money lender.

It is important that you remain calm and not panic when facing preforeclosure. Your credit report should be closely monitored. You should keep in touch with your lender to ensure that you are informed about any potential changes. Pre-foreclosure is not an indicator of foreclosure.

FAQ

What should I look out for in a mortgage broker

People who aren't eligible for traditional mortgages can be helped by a mortgage broker. They look through different lenders to find the best deal. There are some brokers that charge a fee to provide this service. Other brokers offer no-cost services.

How do I calculate my interest rate?

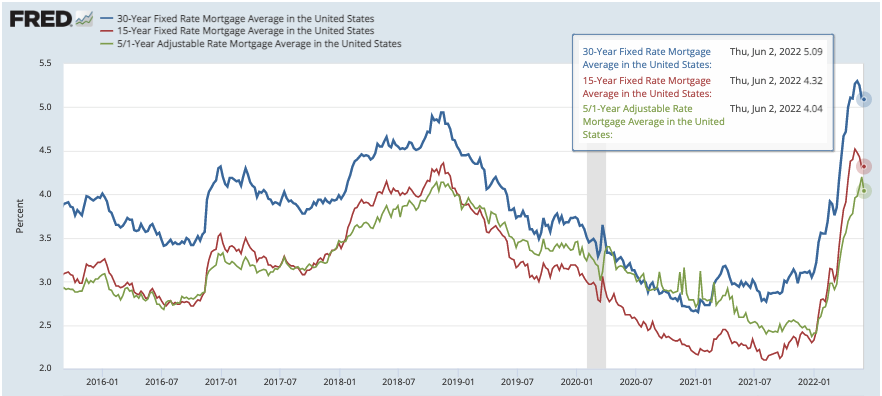

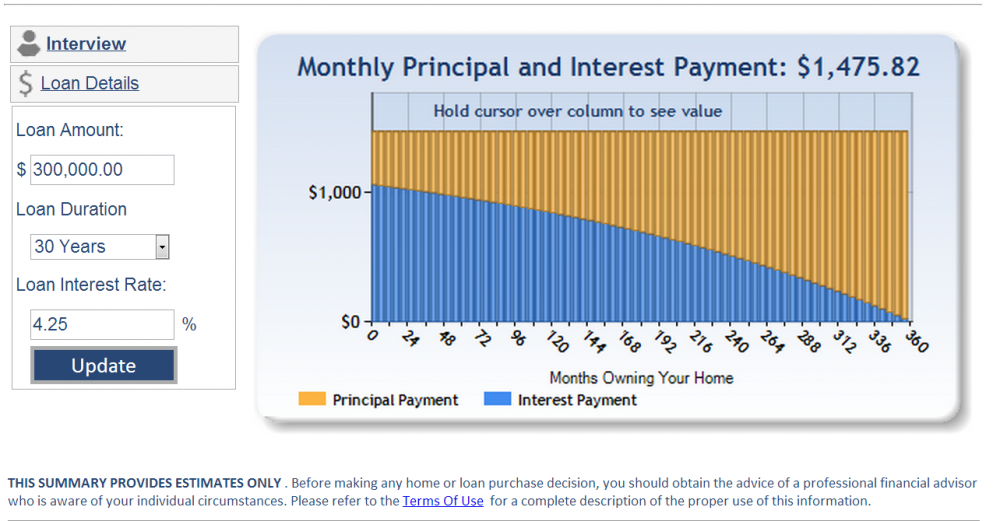

Interest rates change daily based on market conditions. In the last week, the average interest rate was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. For example: If you finance $200,000 over 20 year at 5% per annum, your interest rates are 0.05 x 20% 1% which equals ten base points.

Do I need flood insurance?

Flood Insurance covers flood damage. Flood insurance can protect your belongings as well as your mortgage payments. Learn more about flood coverage here.

How do I repair my roof

Roofs can leak because of wear and tear, poor maintenance, or weather problems. Minor repairs and replacements can be done by roofing contractors. Contact us for more information.

What should I consider when investing my money in real estate

The first step is to make sure you have enough money to buy real estate. If you don’t have the money to invest in real estate, you can borrow money from a bank. It is important to avoid getting into debt as you may not be able pay the loan back if you default.

You also need to make sure that you know how much you can spend on an investment property each month. This amount should include mortgage payments, taxes, insurance and maintenance costs.

Also, make sure that you have a safe area to invest in property. It would be a good idea to live somewhere else while looking for properties.

How much will it cost to replace windows

Windows replacement can be as expensive as $1,500-$3,000 each. The total cost of replacing all of your windows will depend on the exact size, style, and brand of windows you choose.

How can I determine if my home is worth it?

If your asking price is too low, it may be because you aren't pricing your home correctly. Your asking price should be well below the market value to ensure that there is enough interest in your property. To learn more about current market conditions, you can download our free Home Value Report.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to Find a Real Estate Agent

A vital part of the real estate industry is played by real estate agents. They can sell properties and homes as well as provide property management and legal advice. You will find the best real estate agents with experience, knowledge and communication skills. Look online reviews to find qualified professionals and ask family members for recommendations. Consider hiring a local agent who is experienced in your area.

Realtors work with residential property sellers and buyers. The job of a realtor is to assist clients in buying or selling their homes. In addition to helping clients find the perfect house, realtors also assist with negotiating contracts, managing inspections, and coordinating closing costs. A commission fee is usually charged by realtors based on the selling price of the property. Unless the transaction closes, however, some realtors charge no fee.

The National Association of Realtors(r), (NAR), has several types of licensed realtors. To become a member of NAR, licensed realtors must pass a test. A course must be completed and a test taken to become certified realtors. NAR recognizes professionals as accredited realtors who have met certain standards.