It is important to know how a home-equity line of credit works before you consider taking out this loan. This type revolving credit is secured with your home. It has a set interest rate and repayment period. To be approved, you must have equity in your home. The total amount that you owe must be lower than the value of your home. Additionally, your lender will assess your credit score as well as your debt-to income ratio to determine if this type of loan is right for you.

Revolving credit secured with your home

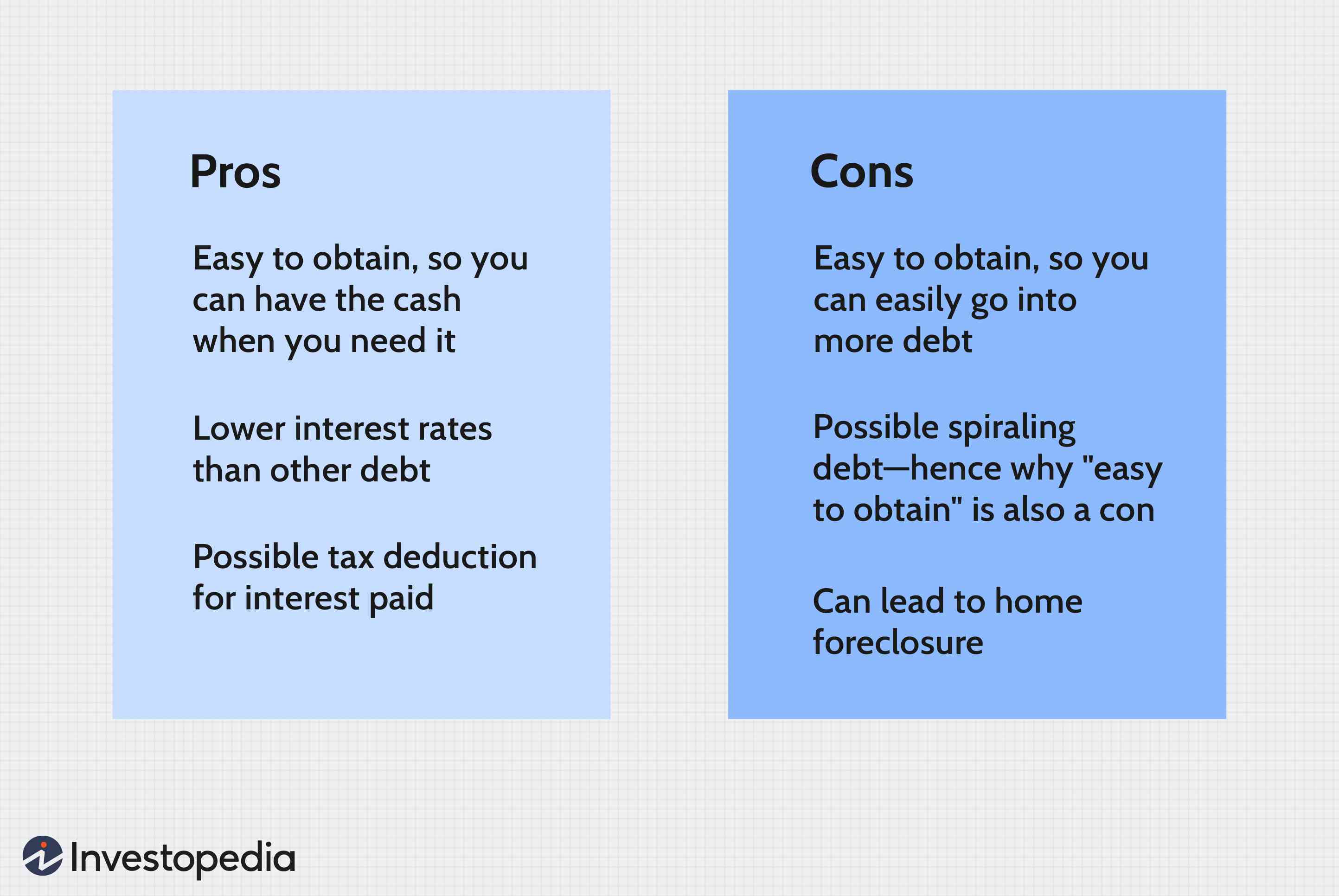

A home equity loan of credit (or HELOC) is a line of credit that allows you to borrow against your equity. This credit can be used to consolidate high-interest debts or pay off large debts. You can also deduct the interest from these loans.

To be eligible for a home equity credit line, you must own your house and have equity available. Your total home equity must not exceed its market value. Lenders will also examine your debt-to–income ratio, credit scores, and history in paying your bills on schedule.

A home equity line of credit can help you pay for major expenses like medical bills, education, and home repairs. Although a line of credit can be used to cover monthly expenses, you should also understand the risks. You should have an emergency fund in place for when you borrow more than you can pay back.

Repayment period

The amount and equity of the home are both factors that will impact the repayment term for a home equity line-of credit. The maximum loan amount is the same for all borrowers. However, the repayment period will vary depending on the amount of the loan and the equity in the home. A quick calculation will allow you to determine the repayment term for a HELOC.

A home equity loan of credit can be repaid in two stages. The first is the draw phase, which typically lasts 10 to fifteen years. During this period, interest and principal payments will be made to the line of credit. The second phase is the repayment period, which begins once the draw period ends.

Each lender will have a different repayment period for a home-equity line of credit. For example, a HELOC may allow you to make interest-only payments during the draw period, and a home equity payment plan may allow you to make principal-and-interest payments after the draw period. This will reduce your monthly payments.

Interest rate

The interest rate on a home-equity line of credit may vary greatly. The margin is determined by several factors, such as the loan to worth ratio, credit qualification and property condition. Typically, the interest rates are lower when the loan first opens, but can increase over time.

The maximum amount you can borrow on a home equity line of credit depends on your home's value, the percentage of home equity that you owe on the mortgage, and your income. A simple calculation will give you an idea about how much you can borrow. If your home's value is 50%, you can borrow up to $20,000.

While a 5-year home equity line credit interest rate may be competitive with other rates in the market, it is better than others. You will still have to pay a monthly fee. Rates are dependent on your credit score. But, those with a loan/to-value ratio greater than 80% will get the lowest rate. A credit score of 740 is required to qualify.

FAQ

What are the advantages of a fixed rate mortgage?

Fixed-rate mortgages allow you to lock in the interest rate throughout the loan's term. This ensures that you don't have to worry if interest rates rise. Fixed-rate loans offer lower payments due to the fact that they're locked for a fixed term.

What are some of the disadvantages of a fixed mortgage rate?

Fixed-rate loans are more expensive than adjustable-rate mortgages because they have higher initial costs. You may also lose a lot if your house is sold before the term ends.

What is a "reverse mortgage"?

A reverse mortgage is a way to borrow money from your home without having to put any equity into the property. It works by allowing you to draw down funds from your home equity while still living there. There are two types to choose from: government-insured or conventional. Conventional reverse mortgages require you to repay the loan amount plus an origination charge. FHA insurance covers your repayments.

How do I calculate my interest rate?

Interest rates change daily based on market conditions. In the last week, the average interest rate was 4.39%. Multiply the length of the loan by the interest rate to calculate the interest rate. If you finance $200,000 for 20 years at 5% annually, your interest rate would be 0.05 x 20 1.1%. This equals ten basis point.

What should you look for in an agent who is a mortgage lender?

A mortgage broker helps people who don't qualify for traditional mortgages. They compare deals from different lenders in order to find the best deal for their clients. Some brokers charge fees for this service. Some brokers offer services for free.

How can I fix my roof

Roofs can become leaky due to wear and tear, weather conditions, or improper maintenance. Roofing contractors can help with minor repairs and replacements. Contact us for further information.

How much money do I need to save before buying a home?

It depends on the length of your stay. Save now if the goal is to stay for at most five years. You don't have too much to worry about if you plan on moving in the next two years.

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

External Links

How To

How to Find a Real Estate Agent

A vital part of the real estate industry is played by real estate agents. They offer advice and help with legal matters, as well selling and managing properties. A good real estate agent should have extensive knowledge in their field and excellent communication skills. For recommendations, check out online reviews and talk to friends and family about finding a qualified professional. It may also make sense to hire a local realtor that specializes in your particular needs.

Realtors work with homeowners and property sellers. A realtor's job is to help clients buy or sell their homes. Apart from helping clients find the perfect house to call their own, realtors help manage inspections, negotiate contracts and coordinate closing costs. Most agents charge a commission fee based upon the sale price. Unless the transaction is completed, however some realtors may not charge any fees.

The National Association of REALTORS(r) (NAR) offers several different types of realtors. Licensed realtors must pass a test and pay fees to become members of NAR. Certified realtors are required to complete a course and pass an exam. NAR has established standards for accredited realtors.