A down payment calculator can be used to calculate how much money is needed to purchase a home. These calculators require information like the location of the property, type of loan, estimated credit score, and the price of the house. Based on your information, they will calculate the down payments. Using a down payment calculator will help you get an idea of what your down payment will be and what kind of budget you should have.

Bankrate's Mortgage Calculator helps you estimate how much money you need to pay for a downpayment

With the help of a mortgage calculator, you can determine how much down payment you will need to purchase your dream home. A higher down payment will result in lower monthly payments and lower risks of getting mortgage insurance. Also, a larger down payment can reduce mortgage fees and interest costs. A mortgage calculator can help make the process easier.

Most people are focused on their down payment. However, it is important that you consider all costs associated with buying a home. This can include insurance, property taxes, homeowners' association fees, and utilities. Using a mortgage calculator can help you figure out these costs and more.

Buying a house with a 20% down payment

Low down payments are possible with many options. Some lenders only require a 3% down payment, while others allow you to make zero down payments. It all depends upon your financial situation and goals. A 3% down payment is sufficient for first-time homebuyers. However, if you require more cash to close the deal, 20% may be required.

Many home sellers prefer homebuyers who have a 20% down payment, as this shows good financial standing and makes finding a mortgage lender easier. You may also have an advantage in a highly competitive market for housing. Not everyone can afford that amount of money, so some people may choose to keep their cash available for other needs.

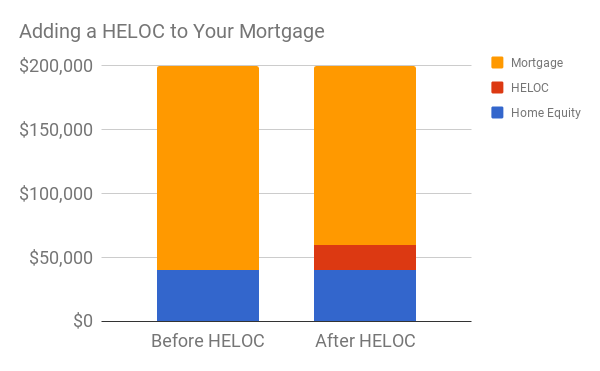

Save for a lower down payment

A smaller down payment is a great way of building equity quicker. Start by determining how much you should save each month. To calculate your monthly expenses, you can use a budgeting tool. You can also consult with a professional financial advisor. After you have established your monthly budget, you will be able to identify areas where you can make savings. First, set aside a certain amount of your monthly income for your downpayment.

You can also save for a smaller downpayment by switching jobs. Although it will take a while for you to establish your budget, once that is done you'll be able set goals and prioritise your expenses you will have no trouble saving more for your downpayment. Americans spend 30 per cent of their monthly earnings on nonmortgage credit, including car loans and credit cards. This means that most of us would have more money to save for a down payment.

Get help from your family and friends

You can save more quickly if you're in a hurry to pay down the down payment. Moving in with your parents or roommates can reduce your living expenses. You can then save money for your down payment. Getting a loan for the down payment can be difficult, however. Higher interest rates and fees will be charged if you require a loan.

With a 20% down payment, you can avoid getting mortgage insurance

Many borrowers believe that paying 20% down is the only way you can avoid private insurance. This requirement is becoming more difficult due to rising home values. Besides, saving up such a large amount of money would delay the opportunity to buy a home for first time buyers and negatively affect the economy.

A piggyback loan is a loan that finance at least 10% of the home's worth to avoid PMI. While this second loan will not have the same terms or interest rate as the first, it can reduce the monthly payments for the mortgage.

FAQ

Is it possible to get a second mortgage?

Yes, but it's advisable to consult a professional when deciding whether or not to obtain one. A second mortgage is typically used to consolidate existing debts or to fund home improvements.

Is it possible for a house to be sold quickly?

It may be possible to quickly sell your house if you are moving out of your current home in the next few months. But there are some important things you need to know before selling your house. You must first find a buyer to negotiate a contract. The second step is to prepare your house for selling. Third, your property must be advertised. Finally, you should accept any offers made to your property.

How much money can I get to buy my house?

This can vary greatly depending on many factors like the condition of your house and how long it's been on the market. Zillow.com shows that the average home sells for $203,000 in the US. This

What are the 3 most important considerations when buying a property?

The three most important factors when buying any type of home are location, price, and size. Location is the location you choose to live. Price refers the amount that you are willing and able to pay for the property. Size refers the area you need.

What is a reverse loan?

A reverse mortgage allows you to borrow money from your house without having to sell any of the equity. It allows you access to your home equity and allow you to live there while drawing down money. There are two types: government-insured and conventional. If you take out a conventional reverse mortgage, the principal amount borrowed must be repaid along with an origination cost. If you choose FHA insurance, the repayment is covered by the federal government.

How long does it usually take to get your mortgage approved?

It depends on several factors including credit score, income and type of loan. It takes approximately 30 days to get a mortgage approved.

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How to Find Houses To Rent

Finding houses to rent is one of the most common tasks for people who want to move into new places. Finding the perfect house can take time. When choosing a house, there are many factors that will influence your decision making process. These factors include the location, size, number and amenities of the rooms, as well as price range.

You can get the best deal by looking early for properties. Also, ask your friends, family, landlords, real-estate agents, and property mangers for recommendations. This will ensure that you have many options.