Know what you're signing before you sign anything on a loan quote. Know that not all loans have the same interest rate cap. It is also important to consider lifetime caps. On the next page of your loan estimate, you will find information about both your lender as well as your loan officer. They can also be reached by phone or email. The last page will show you the total cost for your loan over five year.

Page one

A loan estimate is a brief summary of the costs associated with purchasing a home. It contains details such as the loan terms. It also includes the contact information for the lender. The Loan Estimate information can be used to compare loans from various lenders.

Page 2

The loan estimate contains important information regarding your loan. This document contains details about your monthly payments as well as costs. The first page of a loan estimate should contain the applicant's address and name as well as the price and amount of your loan. All numbers should match. The name and contact information for your mortgage broker should be included on the last page. The place where the loan estimate will be signed should be on the last page.

Page three

The loan estimate will list the total interest, payments, and prepaid charges for the loan. These fees will be reflected in the closing disclosure and are important to compare before signing. The loan estimate will also include the total interest paid and the remaining amount due at the close of the loan.

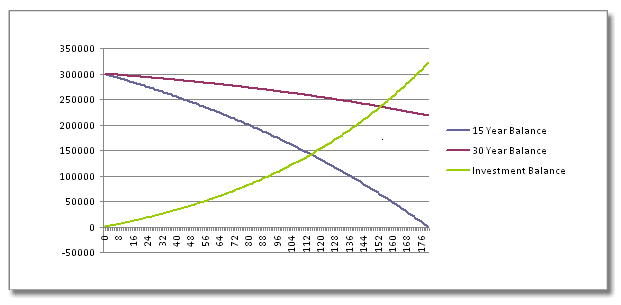

Page four

The loan estimate is an important document that details your payments and other costs. It is usually limited to three pages. On the first page, you will find the terms and conditions. The second page includes details regarding the closing cost. The third page details the loan amount as well as its interest rate. The fourth page contains a breakdown of the mortgage payment. This includes taxes. The loan estimate also lists any prepayment penalties.

Page five

The loan estimate provides important information about the loan. You will learn how much of your loan will be paid off in five years, how much mortgage insurance you will have to pay, and other important details. This will also show you the total interest cost over the loan's term. The total interest percentage is calculated based on the amount you borrow, so make sure you understand it.

Page six

A loan estimate is an important document that details the costs and repayments associated with a loan. The loan estimate begins with a page that includes the applicant's name, address, and property value. These details should be matched with the requested loan amount.

Page seven

A loan estimate is a document that details the terms and costs of a loan. It should contain the applicant's name, address, the value of the property, as well the amount of a loan. You must verify that the loan amount is correct.

Page eight

The breakdown of costs & expenses is an important section of the loan estimate. This information is intended to help homebuyers understand what a loan will cost. The estimate can help you make a comparison and save time.

Page nine

A loan estimate is an important document that details the cost and payment of a loan. It should contain the applicant's name, address, and the price of the property being purchased. It should also include information about the loan terms (if applicable) and the purpose.

Page ten

A Loan Estimate or LES is a document that shows the total cost of a loan. It provides important information regarding the closing costs and interest rate as well as taxes and government fees. It also lists the contact information for your lender. This document is great for comparison shopping.

FAQ

How much should I save before I buy a home?

It depends on how long you plan to live there. If you want to stay for at least five years, you must start saving now. If you plan to move in two years, you don't need to worry as much.

Can I get another mortgage?

Yes. But it's wise to talk to a professional before making a decision about whether or not you want one. A second mortgage is usually used to consolidate existing debts and to finance home improvements.

What should I look out for in a mortgage broker

A mortgage broker helps people who don't qualify for traditional mortgages. They work with a variety of lenders to find the best deal. Some brokers charge fees for this service. Some brokers offer services for free.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How to be a real-estate broker

The first step in becoming a real estate agent is to attend an introductory course where you learn everything there is to know about the industry.

The next thing you need to do is pass a qualifying exam that tests your knowledge of the subject matter. This requires that you study for at most 2 hours per days over 3 months.

You are now ready to take your final exam. You must score at least 80% in order to qualify as a real estate agent.

If you pass all these exams, then you are now qualified to start working as a real estate agent!