To obtain a home-equity line of credit, you will need certain qualifications. You will need to have a minimum credit score of 660, a sufficient income, and a lifetime limit on your HELOC. The lender will also require you to meet their loan-to value and debt-to income ratios.

HELOC applicants must have 660 credits

Good credit is necessary to obtain a HELOC. However, this varies from lender one lender to another. However, most lenders require a credit score of 660 or higher. If your credit score is high, you may be eligible for a reduced interest rate. Lenders will also need proof of income and employment. This information will be used by the lender to calculate your debt/income ratio.

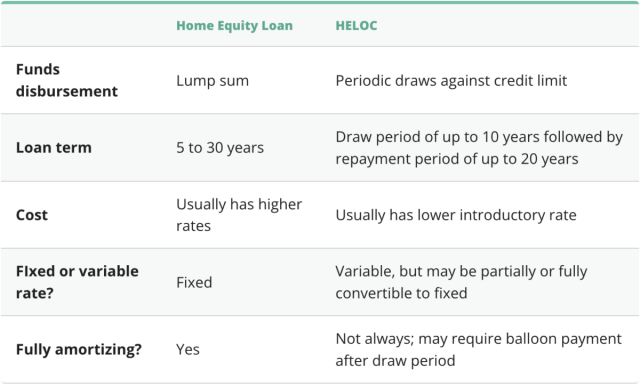

A HELOC can be expensive. Lenders make money by charging fees to cover costs associated with processing the loan. Some lenders charge as much as 6% of the loan amount for closing costs. If you're looking to borrow $100,000 from your home equity you might need to pay $2,000-$6,000 in closing fees. A detailed estimate of closing costs should be provided by your lender.

HELOC loans require an income of at least $20,000

HELOC loans are a loan that you can borrow against your equity. This loan can be obtained from many lenders. There are different requirements that lenders may require to be eligible for this type of loan. You will usually need 15% to 20% equity in the home.

Your credit score affects the amount you can borrow from a HELOC. Your credit score determines your ability and willingness to repay a loan. A higher credit score equals a lower interest. When deciding if you are a risk, lenders look at your payments history. For the best rates, a credit score of 620 and above will suffice.

Lifetime limit on HELOCs

A HELOC (Home Equity Line of Credit) is a type of revolving loan that uses the equity in your home as collateral. This means you can borrow as many as you like and don't have monthly payments. This credit can be used to pay off any credit card or meet any other financial need. The credit line will be paid back in the same way as a credit-card bill. You can also draw it down again and again as you need. As long as the credit is paid back on time and you don't exaggerate your credit, this line of credit can be used as often as necessary.

Your financial documentation is essential before applying for a HELOC. These documents should include proof of income as well as employment. It may also be necessary to pay for a new home valuation. Because home values have increased rapidly in recent years it is possible that you will need to get a new appraisal before applying for a HELOC. The process to close on a HELOC can take from thirty to sixty days, depending on the lender.

Application fee

There are a variety of fees involved with HELOCs. Some lenders charge transaction fees when you withdraw money from the account, and others may charge early termination or inactivity fees. You may also be charged fees if the account is closed prematurely. The fees charged will vary depending on the HELOC type applied for and the lender.

Application fees for a HELOC are typically between $0 and $500. These fees are typically included in the total cost for the loan and can vary greatly. HELOC lenders might also charge loan Origination Fees, which are fees that are related to the HELOC application process. These fees can either be flat-rate or proportional to the amount of credit you receive.

FAQ

How do I repair my roof

Roofs may leak from improper maintenance, age, and weather. Minor repairs and replacements can be done by roofing contractors. Get in touch with us to learn more.

What are the chances of me getting a second mortgage.

However, it is advisable to seek professional advice before deciding whether to get one. A second mortgage is used to consolidate or fund home improvements.

Should I rent or purchase a condo?

Renting is a great option if you are only planning to live in your condo for a short time. Renting will allow you to avoid the monthly maintenance fees and other charges. You can also buy a condo to own the unit. The space is yours to use as you please.

What are the drawbacks of a fixed rate mortgage?

Fixed-rate loans are more expensive than adjustable-rate mortgages because they have higher initial costs. If you decide to sell your house before the term ends, the difference between the sale price of your home and the outstanding balance could result in a significant loss.

What are the advantages of a fixed rate mortgage?

Fixed-rate mortgages allow you to lock in the interest rate throughout the loan's term. This will ensure that there are no rising interest rates. Fixed-rate loans offer lower payments due to the fact that they're locked for a fixed term.

How much money do I need to save before buying a home?

It depends on the length of your stay. Start saving now if your goal is to remain there for at least five more years. But, if your goal is to move within the next two-years, you don’t have to be too concerned.

How much money will I get for my home?

This varies greatly based on several factors, such as the condition of your home and the amount of time it has been on the market. Zillow.com reports that the average selling price of a US home is $203,000. This

Statistics

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

External Links

How To

How to Find an Apartment

The first step in moving to a new location is to find an apartment. Planning and research are necessary for this process. This includes researching the neighborhood, reviewing reviews, and making phone call. You have many options. Some are more difficult than others. The following steps should be considered before renting an apartment.

-

Online and offline data are both required for researching neighborhoods. Online resources include websites such as Yelp, Zillow, Trulia, Realtor.com, etc. Offline sources include local newspapers, real estate agents, landlords, friends, neighbors, and social media.

-

Read reviews of the area you want to live in. Review sites like Yelp, TripAdvisor, and Amazon have detailed reviews of apartments and houses. You can also check out the local library and read articles in local newspapers.

-

To get more information on the area, call people who have lived in it. Ask them what they loved and disliked about the area. Ask if they have any suggestions for great places to live.

-

Consider the rent prices in the areas you're interested in. You might consider renting somewhere more affordable if you anticipate spending most of your money on food. If you are looking to spend a lot on entertainment, then consider moving to a more expensive area.

-

Find out about the apartment complex you'd like to move in. What size is it? What's the price? Is it pet friendly What amenities are there? Can you park near it or do you need to have parking? Are there any rules for tenants?