A home mortgage calculator is an automated tool that helps homeowners calculate the monetary impacts of various variables. It is simple to use and can help homeowners save time and money. A home refinance calculator is a tool that homeowners can use to make informed financial decisions. Entering some basic information will allow you to create a home mortgage calculator that can help you find the best rate possible for your home and within your budget.

Cash-out refinance is tax-free

A cash-out home refinance can be a great way for home improvements to be made without paying taxes. A cash-out refinance will not be free of cost. It is debt, and you will need to pay interest on it. However, under the Tax Cuts and Jobs Act of 2018, you won't have to report the money as income.

Refinances of homes with cash are exempt from taxes because the money is not treated as income. The IRS considers the equity that you receive from a cash-out refinance as an additional loan, rather than cash income. But cash-out home loans have different rules than traditional ones. You can, for example, deduct a certain amount of mortgage points.

Refinance to a more long-term loan term

Refinancing a home can help you lower your monthly payments and get lower interest rates. This may allow you to pay down your mortgage sooner and build equity faster. Refinancing a home can have its advantages and risks. Calculate your monthly mortgage payments using our mortgage calculator.

Consider the loan term length when refinancing your house. You will save thousands of dollars on interest over the term of your loan.

Refinance can bring you tax benefits

If you're planning to refinance your home, you might be wondering if the process has any tax benefits. Refinance fees are not tax-deductible. However the appraised value of your home may be. It could be due to rising property prices, or the fact the appraised value of your home was higher that what the tax authority has assessed.

However, refinancing does come with its share of tax benefits. One benefit is the ability of deducting points from your mortgage. Points are equal to 1% on the loan balance and are deductible over the loan's term. This deduction is applicable to refinance of your primary home or any other qualified property. You can also use your discount points if you refinance to obtain a lower interest rate.

Refinance charges are often common

The common fees associated with a home loan refinance should be known by applicants. A lot of lenders charge an application cost, which can be anywhere from $75 up to $300. The application fee is used to cover administrative costs like assessing loan eligibility. Some lenders also charge a loan origination fee of 0.5% to 1.5% of the loan amount. Additional fees may be charged by lenders for title searches, which can range from $200 to $400.

A loan with an higher interest rate is typically more expensive than one having a lower one. You may be able finance the fees using the remaining balance of your home's equity. Another option is to cash out the funds you've saved. Discuss the costs with your lender when refinancing. Determine if they can be negotiated.

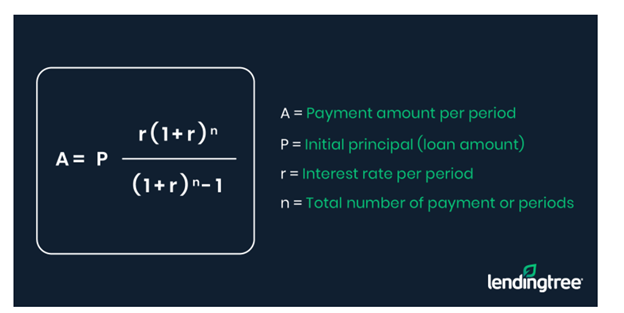

Calculator

A home finance calculator will help you figure out how much you can pay for your home. This calculator will allow you to determine your monthly expenses and the amount that you require for down payments. It will calculate your monthly property taxes, homeowners insurance, and other costs. These costs will be calculated automatically by the calculator in most cases. This makes it as easy and efficient as possible.

Calculator will calculate your monthly payment using your home value, down payment, interest rate and home value. You can either enter a certain amount or a range of money. For example, if you're planning to purchase a $150,000 home, the calculator will calculate the total monthly payment you'll need to pay. Once you know your monthly payment, you can compare different mortgage rates and options.

FAQ

What are some of the disadvantages of a fixed mortgage rate?

Fixed-rate loans have higher initial fees than adjustable-rate ones. A steep loss could also occur if you sell your home before the term ends due to the difference in the sale price and outstanding balance.

Is it better for me to rent or buy?

Renting is typically cheaper than buying your home. However, you should understand that rent is more affordable than buying a house. A home purchase has many advantages. You will be able to have greater control over your life.

What should I consider when investing my money in real estate

The first step is to make sure you have enough money to buy real estate. If you don't have any money saved up for this purpose, you need to borrow from a bank or other financial institution. It is important to avoid getting into debt as you may not be able pay the loan back if you default.

Also, you need to be aware of how much you can invest in an investment property each month. This amount should cover all costs associated with the property, such as mortgage payments and insurance.

It is important to ensure safety in the area you are looking at purchasing an investment property. It is best to live elsewhere while you look at properties.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to buy a mobile home

Mobile homes are houses constructed on wheels and towed behind a vehicle. Mobile homes are popular since World War II. They were originally used by soldiers who lost their homes during wartime. Mobile homes are still popular among those who wish to live in a rural area. These houses come in many sizes and styles. Some houses have small footprints, while others can house multiple families. There are some even made just for pets.

There are two main types for mobile homes. The first type is manufactured at factories where workers assemble them piece by piece. This occurs before delivery to customers. A second option is to build your own mobile house. The first thing you need to do is decide on the size of your mobile home and whether or not it should have plumbing, electricity, or a kitchen stove. You will need to make sure you have the right materials for building the house. Finally, you'll need to get permits to build your new home.

Three things are important to remember when purchasing a mobile house. You might want to consider a larger floor area if you don't have access to a garage. A larger living space is a good option if you plan to move in to your home immediately. Third, you'll probably want to check the condition of the trailer itself. You could have problems down the road if you damage any parts of the frame.

You should determine how much money you are willing to spend before you buy a mobile home. It is important to compare prices across different models and manufacturers. Also, take a look at the condition and age of the trailers. While many dealers offer financing options for their customers, the interest rates charged by lenders can vary widely depending on which lender they are.

You can also rent a mobile home instead of purchasing one. Renting allows you to test drive a particular model without making a commitment. Renting is expensive. Renters usually pay about $300 per month.